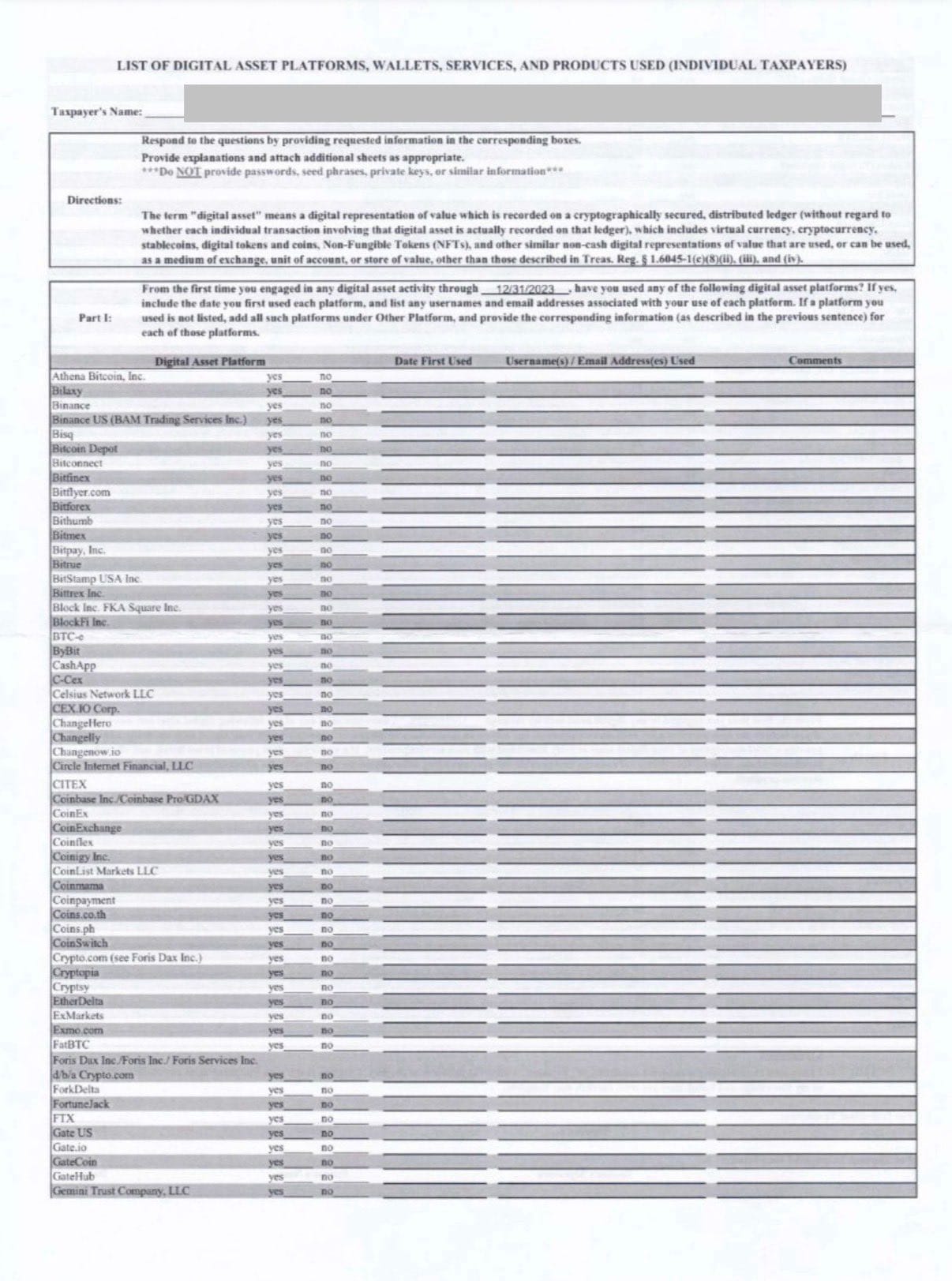

IRS Expands Crypto Audit Rules With Exchange and Wallet Form

A new IRS audit document circulating among tax professionals is drawing sharp attention across crypto after attorney Andrew Gordon published images of the form on social media. The document requires taxpayers to disclose whether they have ever used more than one hundred exchanges, wallets, and service providers, including Coinbase, Binance, and many other platforms. Each entry demands yes or no responses, associated emails, dates of use, and a signed declaration under penalty of perjury, signaling a deeper push to map historical digital asset activity.

Gordon described the form as a sweeping attempt to reconstruct years of crypto movement rather than a narrow review of a single tax period. He warned that forgetting an old account or listing too many platforms could trigger additional scrutiny, while failing to respond at all could lead to a summons. His post framed the document as a strategic tool designed to expand the scope of audits by compelling taxpayers to reveal the full extent of their digital asset footprint.

New enforcement layer tied to 2026 reporting rules

The form aligns with the IRS’s broader digital asset enforcement strategy, which is set to expand significantly in 2026 with the introduction of Form 1099-DA for broker reporting. That rule will require exchanges and certain intermediaries to report customer transactions directly to the agency, creating a standardized data pipeline that did not previously exist. Recent IRS guidance has emphasized that these changes are intended to help the agency trace activity across centralized exchanges, decentralized platforms, and self-custody tools.

Tax professionals say the new audit form appears to function as an investigative instrument rather than a routine verification request. By compelling taxpayers to identify every platform they have touched, the IRS can then request transaction histories, cost basis documentation, and records that may span many years. This approach allows auditors to build a comprehensive map of asset flows, including transfers between personal wallets and third-party services, which historically have been difficult for regulators to track.

The requirement to disclose self-custody tools such as MetaMask and hardware wallets also signals a shift toward examining off-exchange activity. While these tools do not generate traditional account statements, identifying their use gives auditors a starting point to request blockchain addresses, transaction logs, and supporting documentation. For taxpayers who have used multiple platforms over long periods, the process could become time-consuming and complex.

Non-response carries its own risks, as Gordon noted that the IRS can escalate to a summons if a taxpayer ignores the form. That step would compel the production of records and could broaden the inquiry further. For many in the crypto community, the document reflects a growing emphasis on comprehensive reporting and a more aggressive posture toward digital asset enforcement.