How an $8 Billion Gap Brought Down the FTX Crypto Empire

Months before FTX collapsed in November 2022, a telling conversation took place on a paddle court at the Albany resort in the Bahamas. Software developer Adam Yadidia confronted Sam Bankman-Fried with a stark technical finding: once the platform's automated deposit tracking code was corrected in June 2022, it exposed an $8 billion gap between what customers were owed and what the exchange actually held. The trial record makes clear that the eventual collapse was not a liquidity crisis triggered by market panic. The panic simply stripped away the surface to reveal a structural hole that had been built into the system from the start.

FTX projected an image of institutional legitimacy through a carefully constructed public identity. The exchange secured a 19-year naming rights deal for a Miami basketball arena, purchased high-priced Super Bowl advertising slots, and placed its branding on Major League Baseball umpire patches. These moves were not ordinary marketing campaigns but deliberate signals designed to suggest that FTX operated like a regulated financial institution with properly segregated customer funds.

The Personal Brand Behind the Platform

Bankman-Fried reinforced this image through his own carefully managed persona. He cultivated an image of austerity through cargo shorts, unkempt hair, and a Toyota Corolla, projecting the idea of a founder too focused on results to be concerned with personal enrichment. He also tied his identity to Effective Altruism, committing $160 million in grants through the FTX Future Fund to causes such as pandemic preparedness. The brand and the philosophy worked together to manufacture trustworthiness at scale, and that trustworthiness was ultimately the exchange's most valuable asset.

Behind that public image, however, customer funds were being routed through a structure that served the interests of Alameda Research, the hedge fund co-founded by Bankman-Fried. FTX directed customer fiat deposits to Silvergate Bank accounts held by a shell company called North Dimension, which was incorporated as an electronics reseller to disguise its actual function. The company was an Alameda-controlled conduit that funneled customer money into the hedge fund before it ever reached the exchange. Gary Wang, FTX's co-founder, testified that a single switch in the platform's source code exempted Alameda from the same risk engine that would have liquidated any other account with a negative balance, effectively allowing the hedge fund to spend billions in customer funds without triggering any automated safeguard.

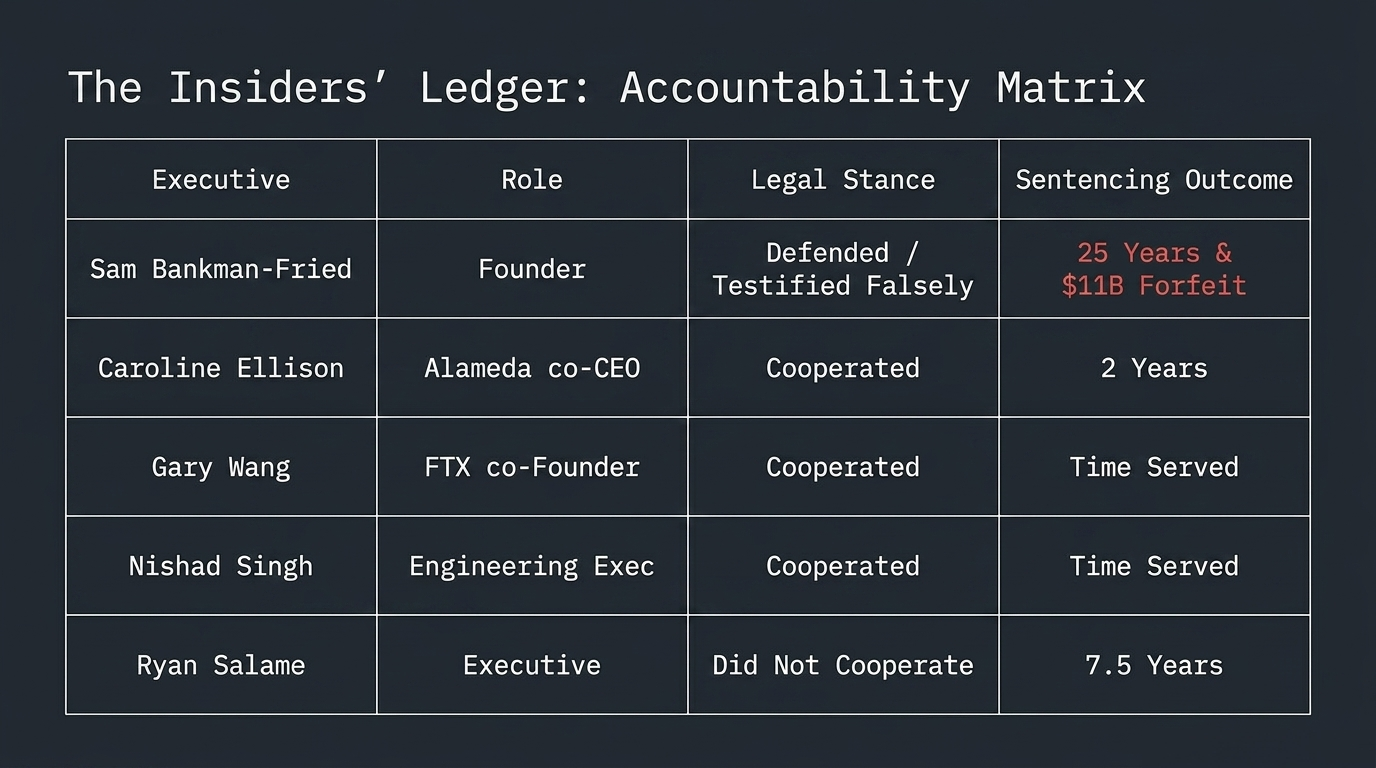

As the internal shortfall grew, the accounting around Alameda became increasingly detached from reality. Caroline Ellison, who led Alameda, testified that she prepared seven alternative versions of the firm's balance sheet in 2022, each engineered to conceal roughly $10 billion in customer-funded liabilities from outside lenders. The November 2022 CoinDesk report that exposed Alameda's heavy reliance on FTT tokens, which FTX had minted itself, did not create the deficit. It simply made the existing one impossible to hide any longer.

The 11-day collapse that followed saw billions in withdrawal requests overwhelm a system that had no reserves to meet them. Nishad Singh, a senior engineering executive at FTX, testified that he felt betrayed after five years of work had turned out to serve such harmful ends. John J. Ray III, the restructuring CEO brought in after the bankruptcy filing, described a complete failure of corporate controls and an absence of reliable financial records. Government forensic accountants traced where the customer funds actually went, finding that $228 million had been spent on Bahamian real estate and $195 million had gone to direct payments to insiders by June 2022 alone.

By spring 2026, a court-approved recovery plan projected repayments of roughly 119 cents on the dollar for most creditors, a figure that has been widely cited as an unexpectedly strong outcome. The reality is more complicated. When the restructuring team first took over, the exchange had approximately 100 Bitcoin remaining on hand. The recovery was made possible largely by the appreciation of venture investments held by the estate, including a $1.3 billion sale of an Anthropic stake, as well as a broad crypto market rally. Creditors are being repaid in U.S. dollars at November 2022 asset prices, not in their original tokens, meaning the estate captured the gains from the subsequent market recovery while creditors were settled out at the bottom. The court has been direct in noting this does not constitute being made whole.

Sam Bankman-Fried is currently serving a 25-year sentence at FCI Terminal Island. His legal team argued an appeal in November 2025, but no opinion has been issued and the conviction remains intact following a court denial of a separate motion for a new trial in April 2026. The FTX case stands as a documented example of how public trust can be systematically manufactured and exploited within financial systems, a pattern that predates crypto and one the industry will need to reckon with as institutional adoption continues to grow.

Sentiment Analysis

Loading market sentiment…