Bitcoin and Crypto Are Challenging the Century Old Federal Reserve System

Few moments in American legislative history carry as much long-term weight as the final weeks of 1913. On December 23 of that year, with most of Congress already home for the Christmas holiday, President Woodrow Wilson signed the Federal Reserve Act into law. Earlier that same year, on February 3, the 16th Amendment had been ratified, permanently establishing the federal income tax. Together, these two measures which passed in the same calendar year, with little public fanfare, fundamentally altered how money works in the United States and who ultimately benefits from its creation.

The groundwork for both had been laid six years earlier during the Panic of 1907, when the American banking system nearly collapsed entirely. Banks in 73 cities suspended payments, and the rescue that followed did not come from any government body. It came from J.P. Morgan, a 70-year-old private banker who gathered the country's most powerful financial leaders in his Madison Avenue library, locked the doors, and refused to let anyone leave until they agreed to fund a collective bailout. This event made it undeniably clear that a single private individual held more sway over the nation's financial fate than any elected official, and the public demand for a formal "system" grew loud enough that Washington could no longer ignore it.

The Secret Meeting That Designed America's Central Bank

What most history books leave out is where the Federal Reserve was actually designed. In November 1910, Senator Nelson Aldrich organized a covert trip to the Jekyll Island Club, an exclusive retreat off the coast of Georgia favored by the country's wealthiest families. The attendees, who included Paul Warburg of Kuhn, Loeb & Co. and Frank Vanderlip of National City Bank, traveled in a private rail car and used only first names to avoid being identified. These men collectively controlled roughly a quarter of the world's total wealth and represented the very financial elite the public believed a new banking law would rein in.

Their concern was not the public good but market share. By 1913, non-national banks made up 71% of all American banks, and the major Wall Street institutions were watching their dominance erode. The bill they drafted at Jekyll Island was designed to function as a central banking cartel, one that could use the authority of government to shield large financial players from competition. Frank Vanderlip later acknowledged that the group understood the legislation would have no chance of passing if Congress knew it had been written by Wall Street representatives. The name chosen for the resulting institution, the "Federal Reserve System," was itself a deliberate piece of political branding. "Federal" lent the impression of government control, "Reserve" suggested fiscal prudence, and "System" implied a decentralized network rather than a singular concentration of power.

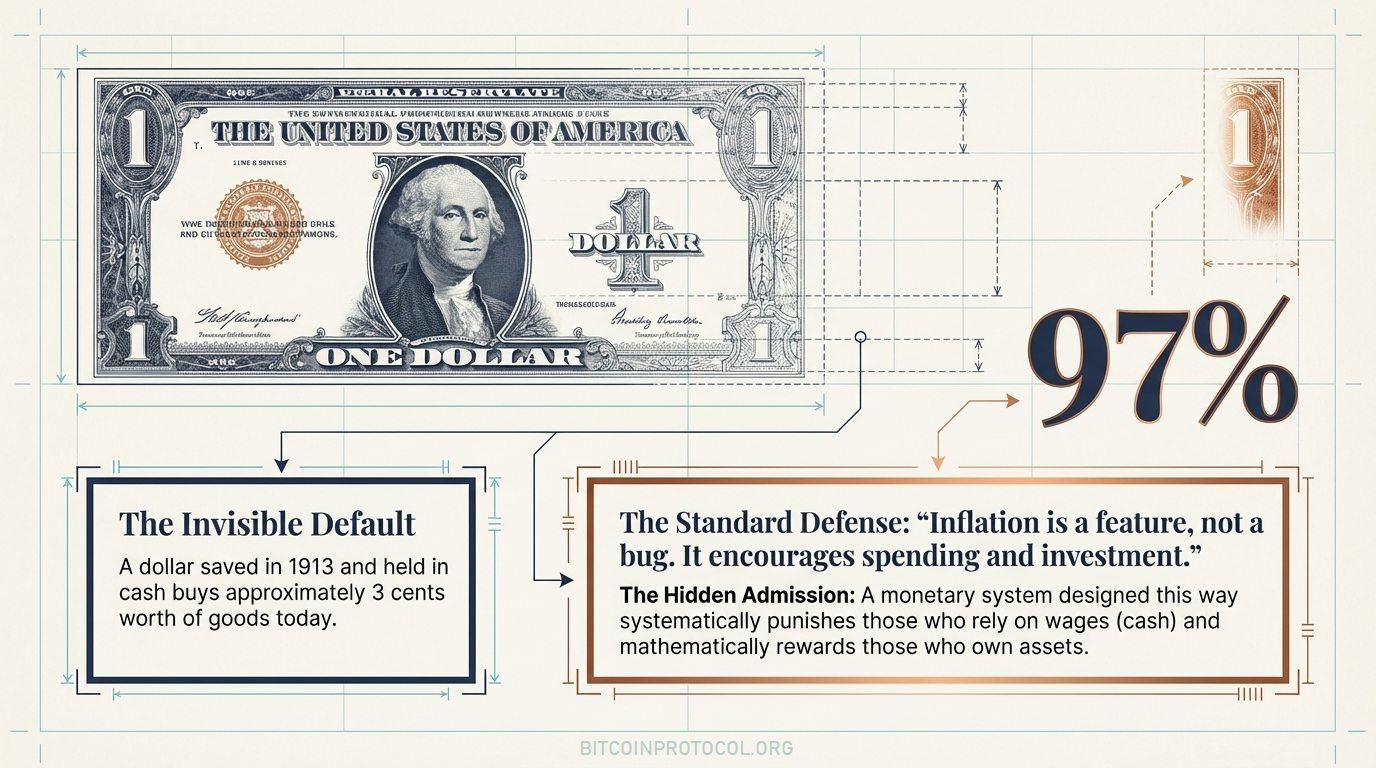

Since its creation, the Federal Reserve has presided over a significant erosion of the dollar's purchasing power. What cost $1 in 1913 now costs roughly $32, representing a loss of approximately 97% of the dollar's original value. The M2 money supply grew from around $4.6 trillion in 2000 to over $19 trillion by 2021, and in 2020 alone, roughly 20% of all U.S. dollars ever created were introduced into circulation. Critics argue this is not a flaw in the system but a built-in feature, one that consistently benefits asset holders like stockholders and real estate investors while gradually eroding the purchasing power of workers who depend on fixed wages and cash savings.

The income tax followed a similar trajectory of mission creep. When the 16th Amendment took effect, the Revenue Act of 1913 exempted all income below $3,000 for single filers, a threshold equivalent to roughly $88,000 in today's dollars for married couples filing jointly. Fewer than 1% of Americans paid any income tax that year, and the top rate sat at just 7%. By 1918, that top rate had climbed to 77%, and by 1944 it reached 94%. The 1942 introduction of payroll withholding, which deducted taxes before workers ever saw their earnings, effectively made the burden invisible and reduced the political friction that might otherwise have slowed its expansion. Milton Friedman, who helped design the withholding system during World War II, later described it as one of the worst things he ever did.

The national debt offers perhaps the starkest illustration of how these two systems interact. In 1913, total federal debt stood at roughly $2.9 billion. Today it exceeds $39 trillion. The Federal Reserve has enabled deficit spending at that scale by keeping interest rates low and serving as a buyer of government bonds, while income tax receipts are used in part to service the interest on that debt. Those interest payments flow from working taxpayers to bondholders, a transfer that critics describe as a permanent structural mechanism for moving wealth from wage earners to capital owners.

Bitcoin and Crypto Emerged as an Answer to Centralized Money

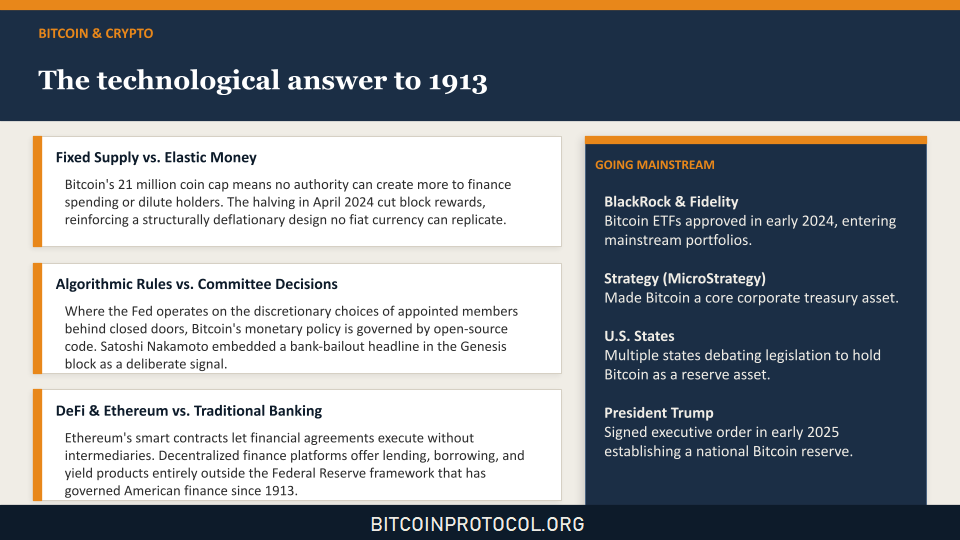

It was precisely this dynamic that Satoshi Nakamoto appeared to be responding to when Bitcoin launched in January 2009, just months after the 2008 financial crisis exposed how fragile the existing system remained. Nakamoto embedded a now famous message in Bitcoin's Genesis block referencing a newspaper headline about bank bailouts, a deliberate signal that the new network was conceived as an alternative to centralized monetary control. Where the Federal Reserve operates on the discretionary decisions of appointed committee members meeting behind closed doors, Bitcoin's monetary policy is governed entirely by open-source code that no single person or authority can alter. Its supply is permanently capped at 21 million coins, meaning no government, institution, or individual can create more of it to finance spending or dilute existing holders.

That fixed supply is what Bitcoin and crypto advocates most frequently cite when drawing a direct line between 1913 and the present. The Fed's ability to expand the money supply at will is, in their view, the root mechanism of wealth transfer that the Jekyll Island architects built into the system. Bitcoin removes that mechanism entirely. Every four years, an event called the halving automatically reduces the rate at which new coins enters circulation, a process written into the Bitcoin protocol itself rather than voted on by any committee. The most recent halving occurred in April 2024, cutting the block reward from 3.125 to 1.5625 Bitcoin, and analysts widely regard these events as structurally deflationary in a way that no fiat currency managed by a central bank can replicate.

The broader cryptocurrency ecosystem has since expanded well beyond Bitcoin, with many digital assets now competing across different use cases. Ethereum introduced programmable smart contracts that allow financial agreements to execute automatically without intermediaries, effectively challenging the role that banks and legal institutions have traditionally played in facilitating transactions. Decentralized finance platforms, commonly known as DeFi, have gone further still, offering lending, borrowing, and yield-generating products that operate entirely outside the traditional banking system. While many of these projects remain speculative and carry risk, they collectively represent a growing infrastructure designed to function independently of the Federal Reserve framework that has governed American finance since 1913.

What makes this moment particularly significant is that institutional adoption of Bitcoin and crypto is no longer a fringe phenomenon. Asset managers including BlackRock and Fidelity now offer Bitcoin exchange-traded funds following regulatory approval in early 2024, bringing the asset class into mainstream retirement and investment portfolios in a way that was unimaginable even five years ago. Publicly traded companies like Strategy have made Bitcoin a core treasury asset, and several U.S. states are actively debating legislation that would allow them to hold Bitcoin as a reserve. President Donald Trump signed an executive order in early 2025 establishing a national Bitcoin reserve, a move that would have seemed politically impossible in any prior administration.

None of this means Bitcoin or cryptocurrency has solved the structural problems encoded in the 1913 legislative framework, and significant challenges remain around volatility, regulatory clarity, and scalability. But the conversation has shifted decisively. A technology that did not exist 16 years ago is now being debated at the highest levels of government as a legitimate alternative to a monetary system that has been in place for over a century.

Whether Bitcoin or another cryptocurrency ultimately fulfills that role or remains one tool among many, its very existence forces a question that the architects of the Federal Reserve never had to answer: what happens to a system built on the control of money when money can no longer be fully controlled?